TLDR / Summary:

- The basic logic: Total costs / productive annual hours, then add profit and risk surcharges

- Productive hours per year: 1,200 to 1,500, not 2,000

- Only 31% of the net charge-out rate accounts for the wage (HWK Stuttgart)

- The 5 most common mistakes and how to avoid them

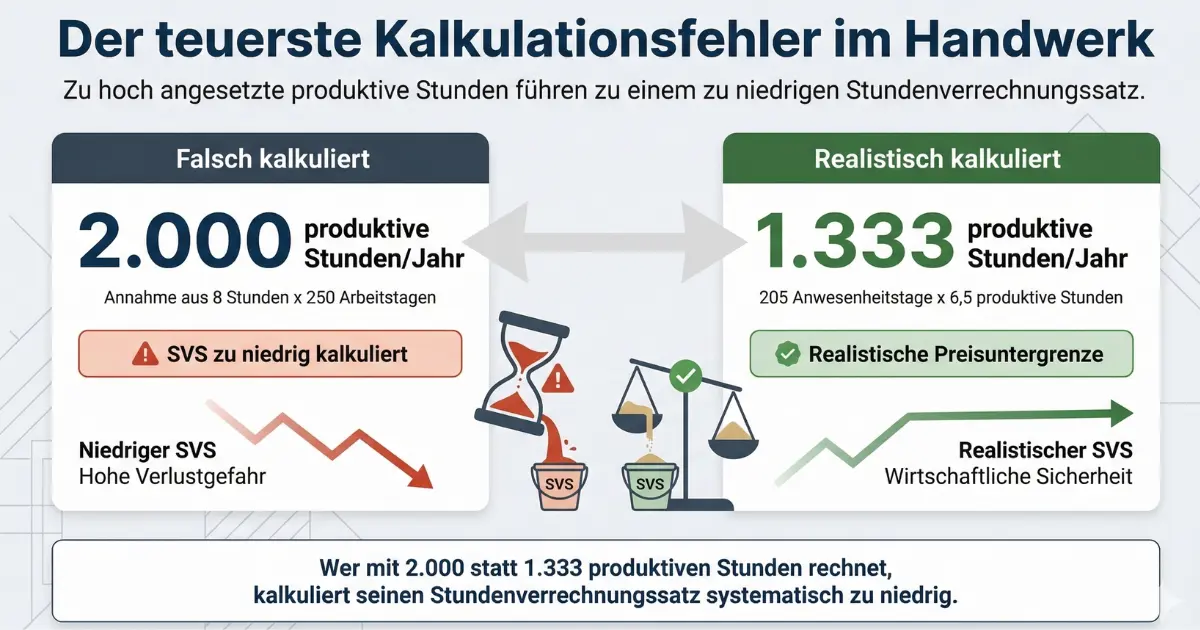

An HVAC business with three journeymen calculates its hourly charge-out rate at 65 euros. Sounds solid. Only: the productive hours were set at 2,000 per year. Realistically, it's 1,350. The actual cost-covering rate is 96 euros. Every hour this business bills at 65 euros generates a loss.

This is not an isolated case. The most common calculation error in craftsmanship is overestimating productive hours (Haufe, 2025). Wrong number of hours = wrong charge-out rate = loss on every order.

Here you will learn how to calculate your hourly charge-out rate correctly, which mistakes you must avoid, and where your trade stands in comparison.

What is the Hourly Charge-Out Rate?

The hourly charge-out rate (SVS) is the price a business must charge per working hour to cover all costs and generate a profit. Not to be confused with the hourly wage.

Hourly wage = what the employee earns. Hourly charge-out rate = what you must charge the customer to work economically. There is a factor of about three between the two numbers.

A sample calculation by the Stuttgart Chamber of Crafts shows how large the difference actually is. The original values are from 2023. The right column is a projection for 2026: The Deutsche Handwerks Zeitung reports an annual increase in journeyman hourly rates of around 5 percent (DHZ, 2024). This results in:

| Position | 2023 (HWK Stuttgart) | 2026 (Projection*) | Share |

|---|---|---|---|

| Gross hourly wage | 20.00 EUR | 23.15 EUR | 31 % |

| Non-wage labor costs | 16.77 EUR | 19.41 EUR | 26 % |

| Operating overheads | 24.52 EUR | 28.38 EUR | 38 % |

| Profit | 3.23 EUR | 3.74 EUR | 5 % |

| Net charge-out rate | 64.52 EUR | 74.68 EUR | 100 % |

| 12.26 EUR | 14.19 EUR | |

| Gross charge-out rate | 76.77 EUR | 88.87 EUR |

*Projection: Original values of the HWK Stuttgart region (as of March 2023), extrapolated with approx. 5 % annual increase over three years (factor 1.158). Actual values may vary depending on trade and region.

The core statement: Only 31 percent of the net charge-out rate is wage. The remaining 69 percent goes into non-wage labor costs, overheads, and profit. This distribution has changed little since 2023.

The Formula

The basic logic:

1. Cost-covering rate = Annual total costs / Productive annual hours

2. Net charge-out rate = Cost-covering rate + Profit surcharge + Risk surcharge

In practice, the calculation consists of five steps:

| Step | What you calculate | Example |

|---|---|---|

| 1 | Gross wage + employer social security contributions (~20-21 %) + other levies = Labor costs/year | 36,000 + 7,560 + 1,800 = 45,360 EUR |

| 2 | Rent + vehicles + insurance + tools + administration = Overhead costs/year | 48,000 EUR |

| 3 | (Labor costs + overhead costs) / productive hours = Cost-covering rate | 93,360 / 1,350 = 69.16 EUR |

| 4 |

| 69.16 + 6.92 + 2.07 = 78.15 EUR |

| 5 |

| 93.00 EUR |

Sources: WHK Controlling (Calculation Scheme), Selbstaendig-im-Handwerk.de (HWK Portal), Haufe (Labor Hourly Rate Calculation in Craftsmanship)

Step 3 is crucial: this is your price floor. Anything below means: you're paying extra. The Deutsche Handwerks Zeitung puts it aptly: "Calculating is in principle nothing other than knowing the price floor" (DHZ, 2024).

Step-by-Step Example Calculation: HVAC Business with 3 Journeymen

Concrete scenario: An HVAC business in North Rhine-Westphalia, three journeymen, the master also works productively.

Labor Costs per Journeyman and Year

| Position | Amount |

|---|---|

| Gross wage (20 EUR/h x 1,720 contract hours) | 34,400 EUR |

| Employer share social security (approx. 20.5 %) | 7,052 EUR |

| Trade association (approx. 4 %) | 1,376 EUR |

| Levies U1, U2, insolvency money | 860 EUR |

| Labor costs per journeyman | 43,688 EUR |

Labor costs for 3 journeymen: 131,064 EUR. In addition, an imputed entrepreneur's wage for the master (here: 55,000 EUR). Those who leave out their own wage are cheating themselves.

Operating Overheads per Year

| Position | Amount |

|---|---|

| Workshop rent + utilities | 14,400 EUR |

| Vehicles (leasing, insurance, fuel) | 18,000 EUR |

| Tools and machinery | 6,000 EUR |

| Insurances (public liability, legal protection) | 4,800 EUR |

| Office, accounting, software | 5,400 EUR |

| Further training | 2,400 EUR |

| Miscellaneous (telephone, advertising, contributions) | 3,600 EUR |

| Total overheads | 54,600 EUR |

Total Costs and Charge-Out Rate

| Position | Amount |

|---|---|

| Labor costs (3 journeymen + master) | 186,064 EUR |

| Overhead costs | 54,600 EUR |

| Total costs | 240,664 EUR |

| Productive hours (4 people x 1,350 h) | 5,400 h |

| Cost-covering rate | 44.57 EUR |

| 4.46 EUR |

| 1.34 EUR |

| Net charge-out rate | 50.37 EUR |

| 9.57 EUR |

| Gross charge-out rate | 59.94 EUR |

In practice, HVAC businesses in 2026 are between 55 and 90 euros net (Turboangebot, 2025). This example business is at the lower end with 50 euros net. The reason: moderate salary level and comparatively low overheads. In Munich or Hamburg, the calculation looks different.

Productive Annual Hours: The Critical Variable

Productive annual hours are the most important factor in the entire calculation. A misestimation of 20 percent changes the charge-out rate by 20 percent. No other item has this leverage.

This is what a realistic calculation looks like:

| Position | Days |

|---|---|

| Calendar days | 365 |

| Weekends | -104 |

| Public holidays (NRW) | -11 |

| Vacation | -30 |

| Sickness (average) | -12 |

| Training | -3 |

| Attendance days | 205 |

| x productive hours per day | x 6.5 |

| Productive annual hours | 1,333 |

Why only 6.5 hours per day? Because travel time to the construction site, setup time, material procurement, cleaning up, and documentation are not billable (yet must still be paid). According to chambers of crafts, productive hours for most businesses range between 1,200 and 1,500 hours per year (WHK Controlling, 2025).

The mistake most people make: 8 hours per day x 250 working days = 2,000 hours. That is 30 to 40 percent too high. A charge-out rate based on 2,000 hours cannot cover the costs.

Hourly Charge-Out Rate by Trade 2026

The following table shows typical net hourly charge-out rates by trade. The ranges arise from regional differences, business size, and specialization.

| Trade | Net SVS 2026 (EUR) |

|---|---|

| Painters and Decorators | 45 to 65 |

| Tilers | 45 to 70 |

| Joiners and Carpenters | 50 to 80 |

| HVAC (Plumbing, Heating, Air Conditioning) | 55 to 90 |

| Electricians | 55 to 85 |

| Roofers | 55 to 85 |

| Automotive Mechatronics | 80 to 150 |

Sources: Turboangebot (Hourly Rate Calculator Craftsmanship), DHZ Price Atlas 2024, handwerk.cloud (Craftsman Hourly Wage 2026)

In eastern Germany, rates are on average 15 percent below the western level (DHZ Price Atlas 2024). In major cities like Munich, Hamburg, or Frankfurt, they are 10 to 20 percent above. You can find a detailed breakdown of hourly rates by trade in our separate post.

The 5 Most Common Calculation Mistakes

1. Productive Hours Set Too High

By far the most common mistake. Those who calculate with 2,000 instead of 1,350 productive hours underestimate their charge-out rate by almost 50 percent. The consequence: every order generates a loss, even if it is paid.

This must be in every calculation: travel times, setup times, administration, sickness, and training must be consistently subtracted. Don't estimate, measure.

2. Forgetting the Entrepreneur's Wage

Many owners do not calculate their own wage (and only notice it when the reserves are used up). The consequence: the master effectively works for free. An imputed entrepreneur's wage of 45,000 to 60,000 euros must be included in the charge-out rate, otherwise the entire calculation is wrong.

3. Underestimating Non-Wage Labor Costs

The pure employer share of social security (pension, health, care, unemployment insurance) is around 20 to 21 percent. But that's not all: in addition, there are trade associations (2-6 percent depending on the trade), and various levies.

In total, non-wage labor costs are often 25 to 30 percent above the gross wage. This fits the HWK Stuttgart example calculation, in which non-wage labor costs make up around 26 percent of the net charge-out rate. Those who only set the social security share of "20 percent" here can easily be 5,000 to 8,000 euros off per employee.

Fact is: record every cost component individually. Flat-rate estimates are not enough.

4. Overheads Set Too Low

The average overhead surcharge in craftsmanship is around 30 percent (handwerk.com, 2025). Many businesses only set 15 to 20 percent. Items like depreciation, proportional office rent, or account management fees are overlooked. This adds up.

The solution is simple: take the BWA (business assessment) of the last twelve months and go through every expense item individually. What is not wage or material belongs in the overheads.

5. No Profit Planned

Cost-covering means: zero profit. No buffer for bad months, no reserves for investments, no growth. A profit surcharge of 5 to 15 percent is not economically optional, but necessary. The same applies to the risk surcharge (2-3 percent): bad debts, warranty work, and unexpected repairs occur in every business.

The Hidden Lever: Reducing Unproductive Hours

The formula clearly shows the connection: more productive hours = lower charge-out rate with same costs. Or to put it another way: every hour an employee spends searching for material, spontaneous trips to the wholesaler, or manual inventory checks drives up the necessary charge-out rate.

A calculation example: a five-person team loses one hour per person per week due to material shortages and unplanned procurement trips. With an hourly rate of 65 euros and 46 productive weeks, that's 14,950 euros per year in wasted capacity.

There are two ways: either increase the charge-out rate (and risk losing orders). Or reduce the unproductive hours. Businesses that systematize their warehousing and control replenishment via automatic reorder point systems win back these hours. Without increasing the price.

Your Charge-Out Rate in Three Sentences

The hourly charge-out rate is not a question of price, but a question of survival. Total costs divided by realistic productive hours (1,200 to 1,500, not 2,000), plus profit and risk. Those who bill below this are paying extra on every order.

Next step: Take your BWA for the last twelve months, calculate the five steps from the formula, and compare the result with your current hourly rate. The difference tells you whether you are working in a cost-covering way.